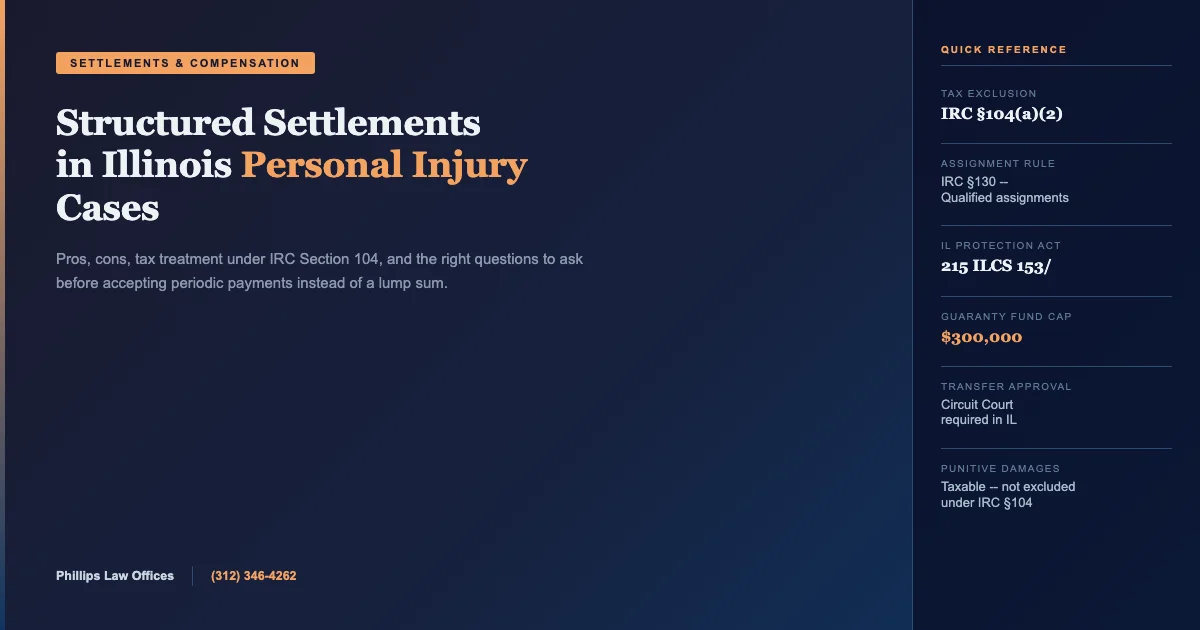

Short answer: A structured settlement is an arrangement in which a personal injury claimant agrees to receive compensation in periodic payments over time instead of a single lump sum. In Illinois personal injury cases, structured settlement payments funded through annuity contracts are generally tax-free under IRC Section 104(a)(2), which excludes compensatory personal injury damages from gross income. The decision to accept a structured settlement versus a lump sum depends on your medical needs, financial situation, and long-term planning goals — and it is a decision you should make only after careful analysis with your attorney and, ideally, an independent financial advisor.

In my experience handling personal injury cases in Illinois, the structured settlement conversation comes up most often in cases with large verdicts or settlements — significant injuries with long-term medical needs, young clients with many decades of life ahead, or situations where the client or their family has concerns about managing a large sum of money at once. There is no universally correct answer. I have seen structured settlements work extremely well for clients who needed guaranteed income to cover ongoing treatment. I have also seen clients later regret not taking the lump sum when unexpected circumstances changed their financial needs. My job is to make sure you understand both options clearly before you sign anything.

How a Structured Settlement Works

When a personal injury case settles, the defendant (or more accurately, the defendant’s insurance company) agrees to fund a structured settlement by purchasing an annuity from a life insurance company. That annuity then makes periodic payments to the injured party according to a schedule negotiated as part of the settlement agreement. Payments can be structured in many ways: monthly payments for life, annual lump sums at specific dates, a combination of immediate and deferred payments, or payments that increase over time to account for inflation and growing medical costs.

Once the annuity is purchased and the settlement is finalized, the payment schedule is generally fixed. The injured party cannot unilaterally change the schedule or demand an early lump sum. There are secondary market companies that purchase structured settlement payment rights, but this involves court approval under Illinois law and typically results in receiving significantly less than the present value of the remaining payments.

Tax Treatment Under IRC Section 104

Section 104(a)(2) of the Internal Revenue Code excludes from gross income the amount of any damages received (whether by suit or agreement) on account of personal physical injuries or physical sickness. This exclusion applies to both lump-sum settlements and structured settlement payments — as long as the payments are funded through a qualified annuity under a structured settlement arrangement that meets the requirements of IRC Section 130. The interest earned inside the annuity is also excluded from income, which is a significant advantage over investing a lump sum where investment gains would generally be taxable.

Punitive damages are taxable regardless of how they are paid. Damages for emotional distress that are not attributable to a physical injury may also be taxable. If your settlement includes multiple components, the tax treatment of each component needs to be analyzed separately.

Advantages of Structured Settlements

- Tax-free income stream under IRC Section 104(a)(2) and 130, including the investment earnings inside the annuity

- Guaranteed payments regardless of investment market performance — no risk of losing principal to market downturns

- Spendthrift protection — creditors generally cannot reach future payments that have not yet been received

- Payments can be tailored to match anticipated medical expenses, therapy costs, and living needs

- Can be designed to pay for education milestones, home purchase, or other future needs at specific dates

- Reduces the pressure of managing a large investment portfolio, which can be particularly important for clients who have never managed significant assets

Disadvantages and Risks

- No flexibility once the annuity is purchased — cannot accelerate payments or draw down principal for emergencies without going to court and selling at a discount

- Payments are fixed in nominal dollars, meaning inflation can erode purchasing power over time unless the schedule includes cost-of-living increases

- If the life insurance company that issued the annuity becomes insolvent, payments may be reduced or delayed (though state guaranty associations provide some protection up to statutory limits)

- The total payout over time is generally higher than a lump sum, but the present value may be lower — defendants sometimes use structured settlements to offer larger nominal amounts while actually paying less in present-value terms

- Does not make sense for clients with significant immediate financial needs, outstanding medical bills, or debts that require quick resolution

Structured settlements work best when the client has stable ongoing medical and living costs that can be projected reliably, and when the client does not have sophisticated investment experience or advisors. They work poorly for clients who have large immediate cash needs, outstanding bills, or who want to invest the settlement proceeds for potentially higher returns. Before agreeing to any structure, I always recommend that clients have the proposed annuity independently evaluated by a financial advisor who does not earn a commission from the sale of the annuity. The defense broker has a financial interest in the transaction — your advisor should not.

Illinois-Specific Considerations

Illinois has enacted the Structured Settlement Protection Act (215 ILCS 153/) to protect claimants who later want to sell or transfer their structured settlement payment rights. Under this law, any transfer of structured settlement payment rights must be approved by an Illinois circuit court, which is required to determine that the transfer is in the best interest of the payee considering the welfare and support of the payee’s dependents. Courts scrutinize these transactions carefully, and factoring companies — which purchase payment streams at a discount — must disclose the effective discount rate and fees involved in the transaction.

Illinois also maintains a strong public policy favoring the finality of structured settlement agreements. If you sign a settlement agreement agreeing to a structured settlement, unwinding that agreement is very difficult. Make sure you understand what you are agreeing to before the settlement is finalized.

| Factor | Lump Sum | Structured Settlement |

|---|---|---|

| Tax treatment | Tax-free (personal injury) | Tax-free, including annuity growth |

| Flexibility | Full — invest or spend as needed | Very limited — schedule is fixed |

| Investment risk | You bear market risk | None — annuity is guaranteed |

| Inflation protection | Depends on how you invest | Limited unless schedule includes increases |

| Immediate cash needs | Fully met | May not cover large immediate needs |

| Insolvency risk | None once received | Risk if annuity issuer fails (mitigated by state guaranty funds) |

| Estate planning | Passes to heirs easily | Depends on annuity terms — some are life-only |

Frequently Asked Questions

Are structured settlements tax-free in Illinois?

Yes, when properly structured. Periodic payments from a qualified structured settlement funded by an annuity are excluded from gross income under IRC Section 104(a)(2) and the assignment provisions of IRC Section 130. This includes the investment earnings that accumulate inside the annuity — an advantage not available when you take a lump sum and invest it yourself. However, the tax exclusion applies only to compensatory personal physical injury damages, not to punitive damages or emotional distress damages unconnected to physical injury.

Can I sell my structured settlement later?

Yes, but it requires court approval under Illinois’s Structured Settlement Protection Act (215 ILCS 153/). An Illinois circuit court must find that the transfer is in your best interest before it can proceed. Factoring companies that purchase payment rights typically offer significantly less than the present value of the remaining payments — sometimes 40% to 60% less. If you are considering selling payments, consulting an attorney before approaching any factoring company is strongly advisable.

What happens if the insurance company goes bankrupt?

The annuity funding a structured settlement is typically issued by a highly rated life insurance company, not by the defendant’s liability insurer. If the annuity issuer becomes insolvent, Illinois’s life and health insurance guaranty association provides coverage up to statutory limits (currently $300,000 per covered claim for structured settlement annuities under 215 ILCS 5/). Payments above that limit could be at risk. This is one reason it is important to negotiate structured settlements funded by financially strong, highly rated insurers.

Who benefits most from a structured settlement?

Structured settlements tend to work best for clients who have predictable long-term medical and living costs, who benefit from the discipline of guaranteed periodic income, who have limited experience managing large investments, and who do not have urgent immediate financial needs that require a large upfront payment. They are particularly common in cases involving minors, where the structured payments provide income security over the child’s lifetime, and in catastrophic injury cases where ongoing medical care costs are substantial and ongoing.

Can I negotiate the payment schedule?

Yes. The payment schedule is negotiated as part of the overall settlement. You can request immediate lump sums followed by periodic payments, annual large payments at specific life milestones, increasing payments over time to account for inflation, or life-contingent payments that continue as long as you live. The defense and their annuity broker will present a proposed schedule, but you and your attorney can counter with a schedule that better fits your actual projected needs. An independent structured settlement consultant can help you analyze the proposals.

Authoritative Sources

- IRC Section 104(a)(2) — Federal exclusion of personal physical injury damages from gross income

- IRC Section 130 — Tax treatment of structured settlement assignment arrangements

- 215 ILCS 5/ — Illinois Insurance Code, including life insurance guaranty association provisions

- 215 ILCS 153/ — Illinois Structured Settlement Protection Act, governing transfer of payment rights

Related Illinois Injury Guides

- Pain and Suffering Damages in Illinois Personal Injury Cases

- Should You Accept the First Settlement Offer in Illinois?

- Are Personal Injury Settlements Taxed in Illinois?

- Recovering Future Medical Expenses in Illinois Personal Injury Cases

If you are evaluating a structured settlement offer in your Illinois personal injury case, contact Phillips Law Offices at (312) 346-4262 for a free consultation. We can help you analyze the proposal and make sure the structure actually serves your long-term interests.