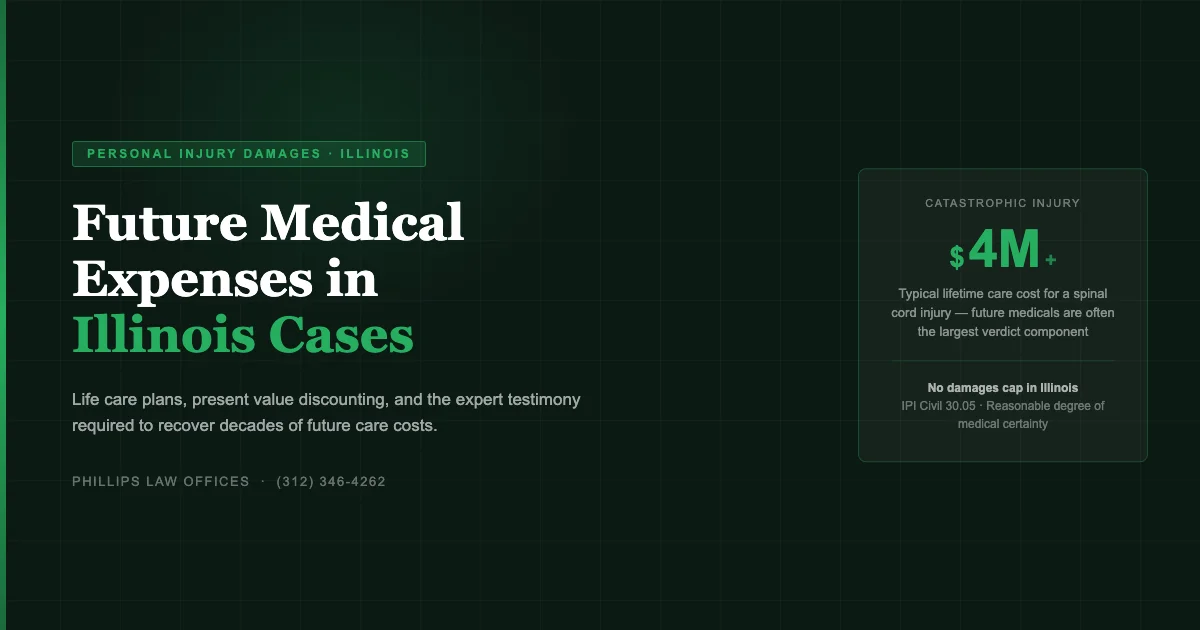

Short answer: Future medical expenses are recoverable in Illinois personal injury cases when proven to a reasonable degree of medical certainty through expert testimony. A life care planner projects the cost and frequency of future treatment, and an economist discounts those costs to present value. For catastrophic injuries, future medicals often represent the largest single component of a settlement or verdict, and Illinois places no cap on compensatory damages, making thorough expert preparation essential to a full recovery.

In my experience handling Illinois catastrophic injury cases, future medical expenses are where verdicts and settlements are made or lost. A client with a spinal cord injury, traumatic brain injury, or severe burn injury may need decades of medical care. If the life care plan is incomplete, challenged successfully by defense experts, or excluded by the trial judge, the plaintiff walks away with a fraction of what full lifetime care actually costs. Getting this element right from the beginning of the case shapes every other decision, including settlement authority and trial strategy.

The Illinois Legal Standard for Future Medical Expenses

Illinois requires that future medical expenses be proven to a “reasonable degree of medical certainty.” This phrase appears in Illinois Pattern Jury Instruction (IPI Civil) 30.05, which instructs the jury to award compensation for medical care reasonably certain to be required in the future.

The standard does not require absolute certainty, but it does require more than speculation. A physician cannot simply say “he might need surgery someday.” The testimony must establish that the future treatment is more probably than not necessary, based on the nature of the injury, the patient’s current condition, and the standard of care for that condition going forward.

Several foundational principles govern this analysis in Illinois:

- Medical necessity must be established by a physician or qualified medical professional. The life care planner projects costs and frequency, but the underlying medical need must be supported by treating or retained physician testimony.

- The expenses must be reasonable in amount. Defense experts routinely challenge the market rates used in life care plans. Counsel must anticipate geographic cost variances and support rates with documented provider charges in the relevant market.

- Future expenses must be reduced to present value. Illinois law requires that lump-sum future damages be discounted to reflect the investment return the plaintiff will earn on the award. An economist performs this calculation, typically using a risk-free discount rate.

The Life Care Planner: The Foundation of the Claim

A certified life care planner (CLCP) is typically a registered nurse, rehabilitation specialist, or physician with specialized training in projecting the lifetime medical and support needs of catastrophically injured individuals. The life care plan is a comprehensive document that itemizes every medical service, piece of equipment, and support need the injured person will require for the rest of their life, along with the projected cost and frequency of each item.

A complete life care plan for a catastrophic injury case addresses:

- Future surgeries: Revision surgeries, hardware removal, spinal fusion, joint replacement, wound closure procedures

- Physical, occupational, and speech therapy: Frequency and duration projections based on the injury type and expected plateau of recovery

- Pain management: Interventional procedures (epidural steroid injections, spinal cord stimulator implantation, intrathecal pump), medications, and specialist visits

- Home health care: Hours per day of skilled nursing, home health aide, or personal care attendant based on activities of daily living deficits

- Durable medical equipment: Power wheelchair, manual wheelchair, hospital bed, communication devices, adaptive equipment, replacement schedules

- Home modifications: Ramp installation, roll-in shower, widened doorways, lift systems

- Prescription medications: Projected formulary, dosages, and cost trends

- Specialist visits: Neurology, physiatry, urology, pulmonology, orthopedics, depending on injury type

- Psychological and psychiatric care: Therapy for adjustment disorder, PTSD, depression commonly accompanying catastrophic injury

- Transportation: Accessible vehicle modification and replacement costs

“The life care plan is not just an exhibit at trial. It is the organizing document for the entire catastrophic injury case. Every deposition question to the treating physicians, every defense expert disclosure, every settlement demand flows from the life care plan. Cases without a thorough life care plan settle for less because the defense knows the plaintiff cannot quantify what their client actually needs.”

Present Value Discounting and the Economist’s Role

Illinois requires that a lump-sum award for future medical expenses be reduced to its present value. The rationale is that a dollar received today, invested at a risk-free rate, will grow to more than a dollar in the future. Awarding the full nominal future cost without discounting would overcompensate the plaintiff.

The economist’s analysis involves:

- Life expectancy: The starting point is the plaintiff’s projected remaining lifespan. Illinois courts use Social Security Administration (SSA) actuarial tables or standard mortality tables unless there is medical evidence of reduced life expectancy due to the injury itself. Spinal cord injuries and severe brain injuries can reduce life expectancy, which the economist must account for.

- Medical cost inflation: Healthcare costs inflate at a rate historically higher than general CPI. The economist projects medical inflation to offset some of the discount, often resulting in a net present value that is close to the nominal total for long-duration care needs.

- Discount rate: Typically the risk-free rate on U.S. Treasury securities. Defense economists favor higher discount rates (reducing the present value); plaintiff economists favor lower rates.

- Replacement cycles: Equipment and home modifications have finite useful lives and must be replaced on schedule. The economist models these replacement costs into the lifetime projection.

Categories of Future Medical Expenses and Documentation

| Category | Examples | How Documented |

|---|---|---|

| Future surgeries | Revision spinal fusion, hardware revision, contracture release | Treating surgeon’s written opinion; life care planner citing surgical necessity |

| Therapy services | PT/OT/speech at specified frequency | Physiatrist or rehabilitation physician opinion; therapy discharge summary projecting ongoing need |

| Pain management | Spinal cord stimulator, intrathecal pump, injections | Pain management physician’s plan; implant and refill cost documentation |

| Home health care | Skilled nursing, home health aide, personal care attendant hours/day | Life care planner citing ADL deficits; occupational therapy functional assessment |

| Durable medical equipment | Power wheelchair, hospital bed, communication device; replacement at 5-year intervals | Vendor quotes; manufacturer replacement schedules; life care planner |

| Home modifications | Ramp, roll-in shower, doorway widening, ceiling lift | Contractor bid; occupational therapy home assessment |

| Medications | Baclofen, Botox injections, spasticity management | Treating physician Rx; pharmacy cost data; life care planner |

| Specialist visits | Annual neurology, quarterly physiatry, urology PRN | Physician opinion on monitoring frequency; standard of care literature |

Tax Treatment and Structured Settlements

Under Internal Revenue Code Section 104(a)(2), compensatory damages received in a personal injury lawsuit are generally excluded from gross income. This exclusion applies to future medical expenses recovered in a lump sum as part of a personal injury settlement or verdict.

Structured settlements offer an additional benefit: because the payments are made over time from an annuity, the full periodic payment, including any investment gain on the annuity principal, retains the IRC 104 tax exclusion. This means a structured settlement providing $10,000 per month for life is entirely tax-free to the recipient, whereas a lump sum invested and earning returns would be partially taxable on the investment income. For catastrophic injury plaintiffs who need decades of tax-free income to fund medical care, structured settlements are often the most financially efficient vehicle.

Illinois does not impose a state income tax on personal injury settlements. The federal exclusion under IRC 104 applies fully.

Illinois-Specific Considerations: No Damages Cap

Illinois does not cap compensatory damages in personal injury cases. The Illinois Supreme Court struck down the legislature’s cap on non-economic damages in medical malpractice cases in Lebron v. Gottlieb Memorial Hospital (2010), holding the cap violated the separation of powers. The same reasoning applies to attempts to cap economic damages like future medicals.

This means that in a catastrophic injury case, a properly supported life care plan totaling $8 million or $12 million can be presented to the jury without any statutory ceiling on recovery. The constraint is proof, not the law. Defense counsel will attack the life care plan through a competing life care planner who disputes the frequency of services or uses lower market rates. The strength of the plaintiff’s experts, and the treating physicians who support the medical necessity opinions, determines how much of the life care plan survives to verdict.

Who qualifies as a life care planner in Illinois?

A certified life care planner (CLCP) typically holds a nursing, rehabilitation counseling, or related healthcare degree and has completed a certification program through the Commission on Health Care Certification or a similar body. Illinois courts do not require a specific credential for admission as an expert, but defendants attack uncertified or less-experienced planners aggressively. Using a CLCP with trial experience in Illinois, and supporting the plan with treating physician opinions on medical necessity, significantly reduces the risk of exclusion.

Can future medical expenses be recovered if I have health insurance?

Yes. Illinois follows the collateral source rule: damages are not reduced because the plaintiff received compensation from a source independent of the defendant, such as health insurance, Medicare, or Medicaid. Future medical expenses are calculated at the reasonable market value of the services, not the discounted rate the insurer would pay. However, Medicare and Medicaid may assert liens on the recovery that must be addressed as part of settlement.

What if the plaintiff is a child injured in Illinois?

Children present unique life care planning challenges because the life expectancy is longer and the injury may affect developmental milestones in ways that compound over time. A brain injury that affects a 6-year-old’s cognitive development has educational, vocational, and lifetime care implications that do not apply to an adult with the same physical injury. Life care planners with pediatric experience and pediatric neuropsychologists are typically needed to capture the full scope of future needs.

How does a structured settlement differ from a lump sum for future medical expenses?

A lump sum gives the plaintiff and their family full control over the funds immediately, with the freedom to invest, spend, or allocate as they see fit. A structured settlement provides guaranteed periodic payments over a specified period or for life, funded by an annuity purchased from a rated life insurance company. Structured settlements are irrevocable once established, so the payment schedule must be designed carefully to match the plaintiff’s projected medical expense timeline. For clients who lack investment expertise or who are at risk of dissipating funds, structured settlements provide security that a lump sum does not.

Can the defendant challenge my life care plan before trial?

Yes. Defendants routinely file Daubert-style motions in Illinois (governed by Frye and now the Illinois Rules of Evidence) to exclude or limit the life care planner’s testimony. Common grounds include: the planner relied on insufficient medical records, the planner is not qualified by education or experience in the plaintiff’s injury type, or the projected costs are not supported by actual market data. Anticipating these challenges by selecting qualified experts and ensuring the plan is grounded in documented treating physician opinions is critical to keeping the full life care plan in front of the jury.

Authoritative Sources

- 735 ILCS 5/2-604, Itemized Verdict Requirement for Damages (Illinois General Assembly)

- 735 ILCS 5/2-622, Affidavit of Merit in Medical Malpractice (Illinois General Assembly)

- SSA Actuarial Life Tables, Used for Life Expectancy at Trial

- IRS Publication 4345, Tax Exclusion for Personal Injury Settlements (IRC 104)

- 735 ILCS 5/, Illinois Code of Civil Procedure (Illinois General Assembly)

Related Illinois Injury Guides

- How Pain and Suffering Damages Are Calculated in Illinois

- Are Personal Injury Settlements Taxed in Illinois?

- Punitive Damages in Illinois Personal Injury Cases

- Timeline of an Illinois Personal Injury Case

For a free consultation about recovering future medical expenses after a catastrophic injury in Illinois, call Phillips Law Offices at (312) 346-4262.